ATTY. CARLO ANGELO T. NEGADO

WITH THE guidance of their accountants and auditors, businesses were able to successfully complete the filing and payment of their taxes with the Bureau of Internal Revenue (BIR) on April 15. As the dust settles on the annual tax filing season, corporations across the board are now turning their attention to another critical deadline: the submission of audited financial statements (AFS) with the Securities and Exchange Commission (SEC).

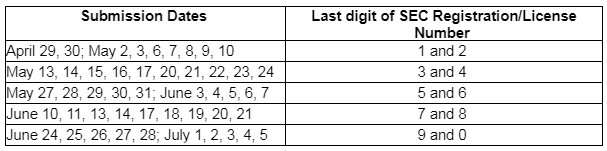

Following the SEC’s thrust for digitalization, the submission of reports over the counter, through mail, or through courier under the SEC Express Nationwide Submission (SENS) facility shall no longer be accepted. All reports must be submitted through the Electronic Filing and Submission Tool (eFAST). In line with past practices aimed at streamlining processes and avoiding congestion in the eFAST, the SEC has once again instituted staggered filing schedules for AFS submissions based on the last numerical digit of the corporation’s SEC registration or license number, as follows:

Corporations must therefore strategize their filings with the SEC based on the window period allotted to them. To avoid delays and unnecessary resubmissions, corporations must also ensure the accuracy of their submitted reports, along with the necessary attachments. For instance, corporations must ensure that the Audited Financial Statements (AFS) submitted to the SEC are stamped as “received” by the BIR or its authorized banks, unless the BIR permits an alternative proof of submission, such as the system-generated Transaction Reference Number for submissions made through the BIR e-AFS system.

Corporations should also ensure that their submissions do not exhibit poor image quality, are not in a horizontal image orientation, and do not contain inaccuracies regarding company profile, period covered, or submission type. Inaccurate or incomplete submissions would be reverted and considered as not filed with the SEC. Additionally, while the eFast platform allows for 24/7 submissions, the SEC only conducts review, acceptance, and reversion from Mondays to Fridays. Submissions made on Saturdays, Sundays, holidays, or during work suspensions will be deemed filed on the subsequent working day.

The late filing or submission of AFS made outside the regular window period allotted will only be accepted by the SEC starting July 8, 2024, and shall be subject to corresponding penalties calculated from the filing deadline.

Last year, the SEC extended an olive branch to non-compliant corporations through an amnesty program, providing them a window of opportunity to rectify violations with reduced penalties. Since its launch in March 2023, the SEC amnesty program has undergone multiple extensions, initially set to conclude on April 30 but subsequently extended to June 30, September 30, and finally, December 31, 2023.

In addition to the amnesty program last year, the SEC has also issued a notice inviting public feedback on the exposure draft of the revised scale of fines and penalties related to non-compliance with reportorial requirements. Notably, the last revision of fines and penalties occurred in 2002, highlighting the significance of the amnesty program and underscoring the need for companies to comply with regulations lest they face increased penalties.

Following the conclusion of the amnesty program, the SEC issued Memorandum Circular (MC) No. 6, Series of 2024 on March 27, 2024, containing the revised scale of fines and penalties covering requests for monitoring received by the SEC beginning April 1, 2024. Earlier in February 2024, the SEC also released the list of 117,885 suspended corporations for failing to comply with their annual reportorial requirements for more than five (5) years, as well as those that commenced their business but subsequently became inoperative for more than five (5) consecutive years.

Under the revised scale of fines and penalties, one person corporations (OPCs) and domestic stock corporations with retained earnings of not more than P100,000 will incur a basic penalty of P5,000 for the late filing of their General Information Sheet (GIS) or AFS, plus P1,000 for every month of continuing violation. The same penalty applies to domestic non-stock corporations with a fund balance or equity of not more than P100,000. The maximum basic penalty of P25,000 applies to those with retained earnings, fund balance, or equity of more than P10,000,000, plus P1,000 for every month of continuing violation.

The stringent penalties imposed for delays underscore the seriousness of meeting filing deadlines and upholding accuracy in reporting. The timely submission of AFS and other reports to the SEC is not just a procedural formality but a fundamental aspect of corporate responsibility and regulatory compliance.

Corporations must ensure the completeness and accuracy of their submissions to avoid delays and penalties. Despite the opportunity provided by the amnesty program to rectify compliance issues with reduced penalties, some corporations chose not to take advantage of this reprieve. Now, faced with the prospect of heightened fines and penalties, these entities serve as a stark reminder of the consequences of non-compliance.

As regulatory scrutiny intensifies and enforcement measures strengthen, corporations must prioritize proactive adherence to filing requirements to mitigate risks as well as maintain transparency and accountability in navigating the constantly evolving regulatory landscape.

Atty. Carlo Angelo T. Negado is a Senior Associate of the Tax Advisory and Compliance at P&A Grant Thornton. One of the leading audit, tax, advisory, and outsourcing firms in the Philippines, P&A Grant Thornton is composed of 29 Partners and 1,500 staff members. We’d like to hear from you! Tweet us: @GrantThorntonPH, like us on Facebook: P&A Grant Thornton, and email your comments to pagrantthornton@ph.gt.com. For more information, visit our website: www.grantthornton.com.ph.